One of the big problems for Tucson Real Estate buyers and sellers to come out of the recent financial crisis is foreclosures and short sales. Foreclosures and short sales affect Tucson Real Estate in many ways. A major impact is the three year waiting period before a new purchase after one experiences such a setback. Some good news is that now Fannie Mae may reduce that waiting period to two years.

I received this story via email:

With the increase in short sales in recent years in the current real estate marketplace, it has been speculated for some time that some of the standards and waiting periods for a homeowner to be able to qualify for a new home loan after a short sale will change.

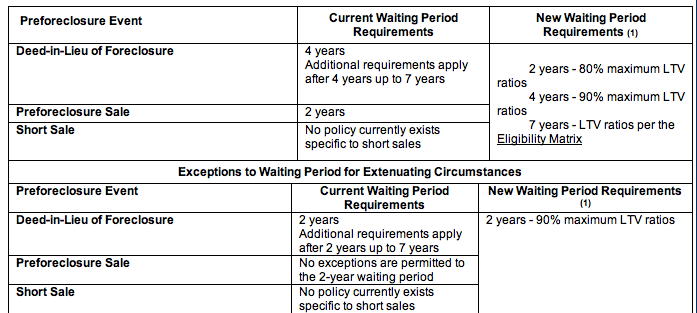

The latest announcement from Fannie Mae does in fact change these standards, as the waiting period for the ability to obtain a new home loan after a short sale or deed in lieu of foreclosure will move be reduced from 4 years to 2 years. However, this rule change does include some caveats as well. The announcement from Fannie Mae states:

“To support overall market stability and reinforce the importance of borrowers working with their servicers when they have difficulty repaying their debt, Fannie Mae is updating several policies regarding the future eligibility of borrowers to obtain a new mortgage loan after experiencing a preforeclosure event (preforeclosure sale, short sale, or deed-in-lieu of foreclosure). The “waiting period” – the amount of time that must elapse after the preforeclosure event – is changing and may be dependent on the LTV ratio for the transaction and whether extenuating circumstances contributed to the borrower’s financial hardship (for example, loss of employment).”

In addition, here are the new specific charts below. They show that, while it is possible to get a new Fannie Mae conventional loan 2 years after a foreclosure, you will need a 20% down payment under normal circumstances of a short sale or a 10% down payment under extenuating circumstances (job loss, etc).

Of course, in addition the borrower must have re-built their credit after the short sale and shown a general good credit history. These new standards go into effect July 1st, 2010 and could serve to help borrowers who experience a difficult situation with the short sale of home to be able to purchase a new home sooner.

This will be the first of perhaps multiple changes we will see in the current market when it comes to qualifying borrowers who have a one time hardship going forward. As more information becomes available we will of course share that information with you.

* I received the above information from http://www.strategicmtgaz.com.

So if you have been affected by a financial setback during these rough times, you no longer have to wait three years to purchase your new Tucson Real Estate.

{kind=link}